A new NACFE confidence report recommends that more fleets explore and spec lightweighting technologies to improve their efficiency, which could help drive down lightweighting technology costs, expand payloads, reduce congestion, and save fleets money.

As fleets and OEMs add more fuel-efficiency technologies, emission reductions and driver amenities to trucks, tractors and trailers, it’s making equipment heavier. Despite this, lightweighting has not been a priority for most fleets in the U.S.

A new Lightweighting Confidence Report published in February by the North American Council for Freight Efficiency (NACFE) recommends more fleets explore and spec lightweighting technologies to improve efficiency. If more fleets start to push for lighter material options from truck makers, it could drive down costs of the more expensive material and help popularize lightweighting across the industry, according to Michael Roeth, NACFE’s executive director, who recently spoke with FleetOwner about the report.

Lightweighting can be achieved by using lighter materials in various parts of tractors and trailers, such as the powertrain, axle suspensions, wheel ends, driveshaft, frame, and fifth wheel.

It’s been more than five years since NACFE’s last Lightweighting Confidence Report. Since that 2015 report, trucks and trailers have gotten heavier, Roeth noted. “Just adding fuel economy technologies — such as aerodynamics — added weight,” he said, adding that emissions regulations, fuel economy features and the push to increase in-cab amenities for drivers has added another 1,000 lbs. to the average tractor-trailer.

Roeth also noted that the growing push for battery-electric trucks, which are even heavier than their diesel counterparts, could help trucking more fully embrace lightweighting technologies. Batteries can add 2,500 to 5,000 lbs. to a truck for the same duty cycle as diesel.

Driven by bulk carriers — which tend to max out their payloads more than reefer and dry vans — that have invested more in lightweighting, the industry has found more ways to free up weight, according to NACFE.

The confidence report divides the freight market into three categories based on how heavy the trucks typically travel:

- Category 1: Trucks that currently travel at the 80,000-lb. limit at some point along nearly 100% of their routes. This represents a small percentage of the industry (about 2%). These are often bulk carriers.

- Category 2: Trucks that are loaded to the maximum weight of 80,000 lbs. (gross-out) on 10% to the majority of their trips. This represents about 10% of the trucks on the road, mostly refrigerator units but also some dry vans.

- Category 3: Dry van units that rarely (approximately 2% of the time) or never travel at maximum weight, either because the goods fill the trailer volume (cube-out) before they gross-out, or simply because their routes and cargo patterns are not conducive to traveling full. About 88% of the trucking industry falls into this category.

Because bulk haulers that travel at the 80,000-lb. limit make up a small percentage of tractor-trailers on the road, there is less demand for expensive lightweighting technologies — such as lighter crossmembers, bracketry and bumpers — which has kept the costs of those components higher. But if other segments start focusing more on lightweighting, it could create better lightweighting economies, Roeth explained.

“If those (lightweighting components) start to increase in popularity at the truck builders, they may be able to lower their price of that optional feature,” Roeth told FleetOwner. “Ultimately, they may even make that their standard. That’s just how this works in the industry — if you have enough buyers, they’ll make it the standard. Maybe they end up making a steel crossmember an option while an aluminum crossmember is standard. Then, with that scale comes better pricing and better availability. That’s a very common pathway in the industry.”

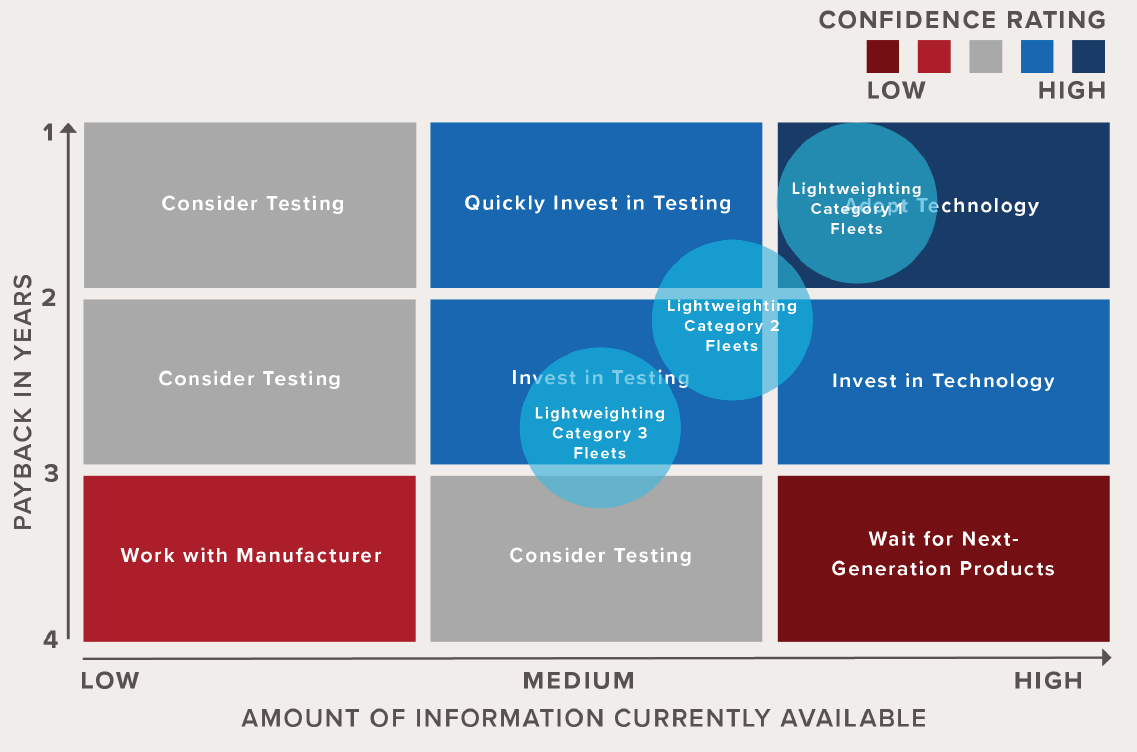

NACFE’s Lightweighting Confidence Matrix illustrates its study team’s confidence in the investment case for lightweighting technologies for each of the three categories of fleets. Category 1 are bulk fleets that gross-out on every trip. Category 2 are reefer and dry van fleets that gross-out on some trips. Category 3 are reefer and dry van fleets that rarely gross-out.Chart: NACFE

But Roeth credited truck builders for trying to keep up with the added weight over recent years. “Their base truck — if there is such a thing as a standard truck — have improved in weight. That’s a big deal,” he said. “One thing that we’re a little concerned about is the optional lightweight features fleets are not buying unless they’re tankers or hauling beverages or those that really need them. We were surprised when we updated this report that more fleets weren’t opting for lightweighting features — particularly those that occasionally gross-out. We thought that would have happened by now, but it really hasn’t.”

Two emerging equipment types embracing lightweighting out of near necessity are battery-electric and hydrogen-powered trucks. Because those technologies add up to 5,000 lbs. to a vehicle, Roeth believes they will help make lightweighting ideas more popular across the industry. “You’re starting to see that happen at Tesla, Nikola, and even the traditional manufacturers who are working to optimize their electric trucks — not just to have a sort of modified diesel truck.”

Trucks can achieve about 2,000 lbs. of weight reduction by investing in a limited degree of lightweight technologies — while more aggressive investment can yield around 4,000 lbs. of savings, according to the report. Bulk haulers take the most advantage of this. Adding 4,000 lbs. to each trip’s payload could remove one in every 11 trucks from the road. This has more than a few benefits, including less congestion on U.S. highways.

Those Category 1 fleets, which make up 2% of the industry, are willing to pay $6 to $11 for every pound of weight a technology will save them, according to the report. Because of how much they value lightweighting, Category 1 fleets have already adopted most of the available technologies. While the other two segments haven’t invested in lightweighting as much, NACFE has noted new trends that suggest lightweighting should be given more attention and is a worthwhile investment for some fleets in Categories 2 and 3.

Here are some lightweighting trend highlights, based on NACFE surveys of fleets and OEMs, from the report:

- Along with tractors and trailers becoming heavier over the past five years, freight is becoming denser and shippers are loading more pallets per trailer.

- Over the next decade, NACFE anticipates more shippers will request Category 2 and 3 trucks to double the times they gross out their payloads, which would be 20% of the time for Category 2 and 4% for Category 3.

- To meet these future demands, Category 2 and 3 fleets would have two options: add more trucks to the road or explore lightweighting

- While lightweighting can be expensive, it is cheaper than running additional trucks on just 10% of routes, according to NACFE.

- Lightweighting to keep a single additional vehicle off the road can save a fleet $1 million over five years. NACFE calculates this savings based on a new tractor costing $120,000 upfront and $1.65 per mile to operate an average of 100,000 miles per year.

- With the industry averaging just under 6 mpg, one less truck means reduced CO2 emissions of nearly 380,000 lbs. per year.

The NACFE Lightweighting confidence report is now available.

By Josh Fisher

CUT COTS OF THE FLEET WITH OUR AUDIT PROGRAM

The audit is a key tool to know the overall status and provide the analysis, the assessment, the advice, the suggestions and the actions to take in order to cut costs and increase the efficiency and efficacy of the fleet. We propose the following fleet management audit.